SpaceX Profitability Trends 2026

A leading aerospace firm shifts from launch fees to subscription services, driving record margins, subscriber surge and a historic IPO bid.

SpaceX is on track to redefine the aerospace industry in 2026 with record-breaking profits and ambitious growth plans. Here's what you need to know:

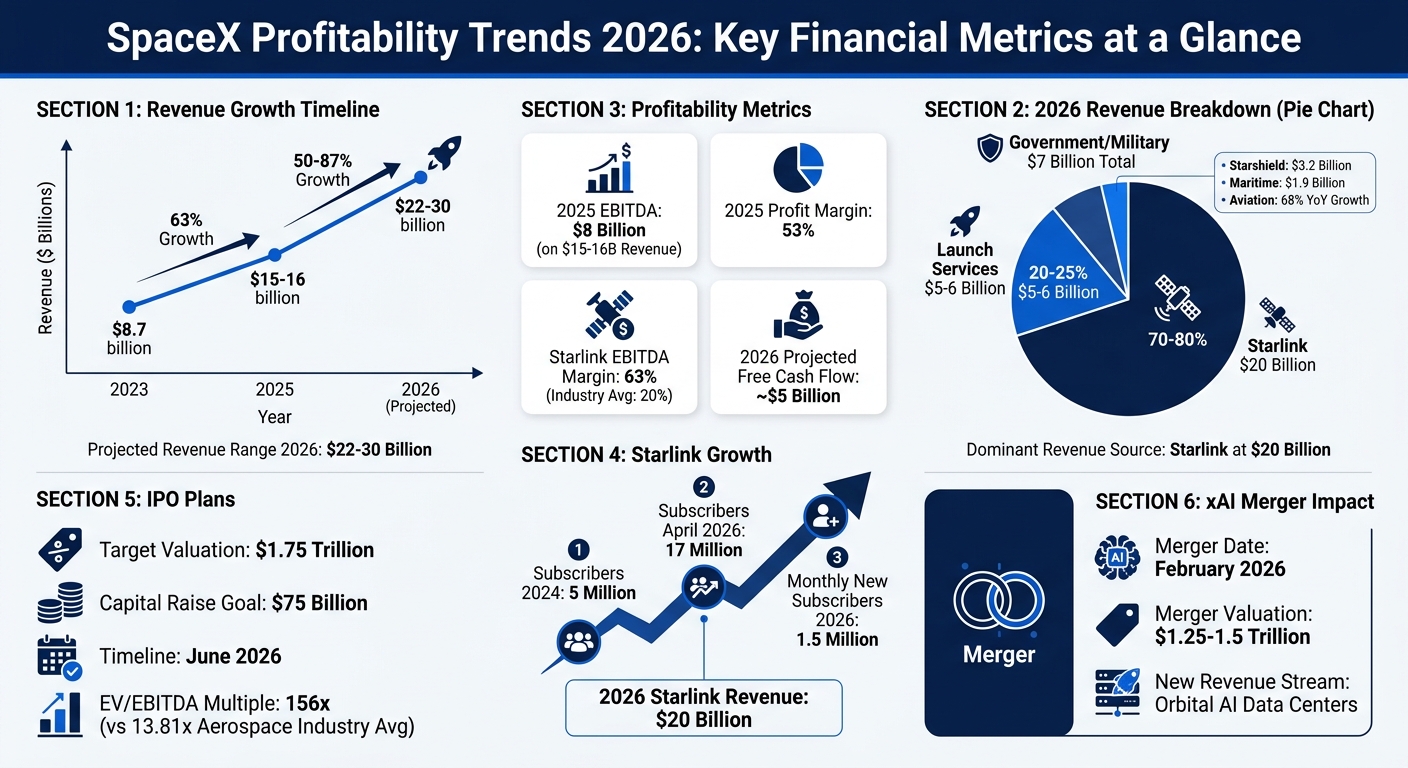

- 2025 Financials: $8 billion in EBITDA on $15–$16 billion revenue, with a 53% profit margin.

- 2026 Projections: Revenue expected to hit $22–$30 billion, driven by Starlink's dominance (70–80% of total revenue).

- Starlink Growth: Subscriber base surged from 5 million in 2024 to 17 million by April 2026, generating $20 billion in revenue.

- IPO Plans: Aiming for a $1.75 trillion valuation in June 2026, targeting a $75 billion capital raise.

- xAI Merger: February 2026 merger valued at $1.25–$1.5 trillion, opening new AI-driven revenue streams like orbital data centers.

SpaceX's shift from one-time launch revenue to subscription-based models is fueling rapid growth, but significant capital demands and execution risks remain. The June IPO could make history, but investors looking for ways to invest in SpaceX must weigh the high valuation against the company's ambitious roadmap.

SpaceX Revenue Growth and Profitability Metrics 2025-2026

2026 Revenue Overview: Main Sources and Results

Revenue Breakdown: Starlink, Launch Services, and New Markets

After achieving notable profitability milestones in 2025, SpaceX's 2026 revenue figures showcase how diversified income streams are fueling continued growth.

In 2026, SpaceX's total revenue is projected to land between $22 billion and $30 billion, a significant jump from the $15–$16 billion recorded in 2025. This increase is largely driven by Starlink, which not only dominated the revenue mix but also nearly doubled its earnings compared to the previous year. Starlink is expected to account for 70% to 80% of total revenue, generating about $20 billion, up from $11.8 billion in 2025. This growth stems from a surge in new subscribers, with the service adding between 750,000 and 1.5 million new users per month throughout the year.

While SpaceX's launch services still control 82% of the global commercial market, their share of the company’s total revenue has decreased. In 2026, launch services are expected to contribute 20%–25%, equating to approximately $5–$6 billion. Government and military contracts, including the Starshield program, are projected to bring in around $7 billion, with Starshield alone contributing $3.2 billion.

New markets have also begun to make a noticeable impact. For example, maritime installations are expected to generate $1.9 billion from about 75,000 shipping vessels, while aviation-related revenue is predicted to grow by 68% year-over-year.

Adding to this, SpaceX's merger with xAI in February 2026 introduced a completely new revenue opportunity: space-based AI infrastructure services. This venture includes plans to deploy a constellation of 1 million solar-powered AI data center satellites. Elon Musk emphasized the shift in revenue sources, stating:

"NASA will contribute only 5% of SpaceX's revenue this year... the vast majority of revenue is from the commercial Starlink system".

Year-Over-Year Revenue Growth

The year-over-year analysis highlights the rapid pace of SpaceX's expansion, driven by its strategic focus on recurring revenue streams.

From 2023 to 2025, SpaceX’s revenue grew by 63%, climbing from $8.7 billion to $15.5 billion. Projections for 2026 suggest an additional increase of 50% to 87% over 2025 levels, marking one of the fastest growth periods in aerospace history.

This growth reflects a deliberate pivot from one-time launch services to subscription-based models with higher margins. In 2025, SpaceX completed 167 launches, but launch revenue grew by just 8%, reaching $4.1 billion. Meanwhile, Starlink’s subscriber base expanded dramatically, growing from 5 million in late 2024 to 10 million by February 2026. The service is adding 1.5 million new customers monthly in 2026. Additionally, Starlink has significantly improved its profitability, with its EBITDA margin climbing from 41% in 2023 to 63% in 2025. This performance far exceeds the margins of traditional satellite operators, which typically hover around 20%.

Stephanie Bednarek, SpaceX's VP of Commercial Sales, provided insight into the company’s future direction:

"2025 and 2026 are likely to represent the peak of Falcon launch activity, with the company planning to progressively shift missions to Starship as the next-generation vehicle matures".

This transition to Starship, combined with new ventures like AI infrastructure and specialized B2B markets, has not only diversified revenue streams but also accelerated growth in existing ones. These developments position SpaceX for sustained revenue growth well beyond 2026, setting the stage for deeper profitability analysis and insights on how to buy SpaceX stock in the next section.

sbb-itb-6fb0794

Profitability Metrics and Industry Comparisons

EBITDA Margins and Total Earnings

SpaceX's financial performance in 2026 underscores its unique business model. Starlink has emerged as the company's financial powerhouse, boasting a 63% EBITDA margin in 2025 and contributing $7.2 billion in adjusted EBITDA from $11.4 billion in revenue. Looking ahead, Starlink's 2026 adjusted EBITDA is expected to climb to nearly $11 billion, supported by $15.9 billion in revenue. This keeps its margins firmly in the 60%–70% range, fueled by ongoing subscriber growth.

In 2025, SpaceX's overall performance saw an EBITDA of approximately $8 billion on $15.6 billion in revenue, translating to a 53% margin. This success is largely credited to Starlink's subscription-based model, which mirrors the efficiency of software-as-a-service operations with low marginal costs. On the other hand, the rocket launch and AI divisions remain highly capital-intensive, with the rocket business alone incurring a negative free cash flow of around $3 billion in 2025.

Despite these capital challenges, SpaceX achieved a key milestone in 2025 by turning cash-flow positive. Projections for 2026 suggest free cash flow could approach $5 billion, thanks to Starlink's steady revenue stream and reduced capital expenditures as the satellite network nears completion.

These impressive margins and cash flow metrics shed light on why SpaceX commands a valuation significantly higher than industry norms.

Comparison to Industry Standards

When compared to industry benchmarks, SpaceX's profitability metrics and valuation multiples stand out dramatically. The company's $1.25 trillion valuation translates to an EV/EBITDA multiple of 156x based on 2025 data. This far exceeds the average multiples in related sectors: aerospace and defense at 13.81x EBITDA, internet services at 14.56x, and even the broader tech sector at 21.42x.

| Metric (Est. 2025/2026) | SpaceX | Aerospace/Defense Benchmark | Internet Services Benchmark |

|---|---|---|---|

| EV/EBITDA Multiple | 156x | 13.81x | 14.56x |

| EV/Sales Multiple | 81x | 1.84x | 4.12x |

| Starlink EBITDA Margin | 63% | N/A | ~20–30% (Typical) |

| Launch Operating Margin | 40% (Projected) | ~10–15% (Typical) | N/A |

This valuation premium reflects the market's confidence in SpaceX's operational strengths. The company manufactures about 85% of its hardware in-house, minimizing reliance on suppliers and supporting its high-margin operations. Additionally, SpaceX held a commanding 82% share of the global commercial launch market in 2025, largely due to its reusable rockets. These rockets bring launch costs down to roughly $30 million per mission, which is about 10 times cheaper than traditional expendable rockets.

"SpaceX has established such a robust and long-standing cost advantage over its competitors... that it had a market share in excess of 80% of the launch market in 2025."

This insight from Aswath Damodaran, Professor of Finance at NYU Stern, highlights the strategic edge SpaceX has cultivated. These financial and operational achievements align with its projected growth trajectory for 2026, reinforcing investor confidence in the company's long-term potential. This confidence is driving interest in pre-IPO stock opportunities, though investors must remain vigilant against fraud.

Analyst Reveals ❗What the SpaceX IPO is Worth?

Main Revenue Drivers and Profit Boosters

SpaceX's impressive revenue performance is powered by several key factors that are driving its profit growth. Let’s dive into what’s fueling this momentum.

Starlink's Subscriber Growth and Revenue Contribution

Starlink has become the backbone of SpaceX's cash flow. In 2026, the service is adding 1.5 million new users per month - double the pace seen in 2025, when monthly additions were at 750,000. By the end of the year, Starlink is projected to reach between 16.8 million and 18 million subscribers. This growth translates into an expected $20 billion in revenue for 2026.

Starlink’s revenue streams are diverse, spanning consumer, government, maritime, and enterprise sectors. Here’s a breakdown of the 2026 revenue forecast:

- Consumer services: $11.3 billion

- Starshield (government contracts): $3.2 billion

- Maritime services: $1.94 billion

- Enterprise accounts: $1.68 billion

Additionally, aviation revenue is up by 68% this year, with recurring subscriptions contributing about 85% of consumer revenue.

"Starlink is delivering data capacity previously unattainable, attracting a broad customer base, including urban users."

- Chris Quilty, Satellite and Space Analyst, Quilty Space

Starlink is also expected to generate $14 billion in EBITDA and $8.1 billion in pro forma free cash flow in 2026. SpaceX has ramped up its satellite manufacturing to over 4,000 units annually - around 340 per month - a 40% increase from 2024 levels. On top of that, the new Direct-to-Cell mobile service is projected to reach 25 million monthly active users by the end of the year, creating a fresh revenue stream by integrating satellite connectivity into smartphones. This shift underscores SpaceX's pivot from one-off launch revenues to sustainable subscription-based income.

Falcon 9 and Starship Launch Services

While Starlink dominates, SpaceX's launch services remain a critical pillar of its business. In 2025, Falcon 9 achieved an impressive 165–166 launches with a 99.53% success rate, generating $4.1–$4.4 billion and capturing 82% of the global commercial launch market.

That said, revenue growth from launch services has slowed to an estimated 5–8% year-over-year. This is partly because SpaceX is prioritizing internal Starlink deployments over external commercial contracts. The internal cost of Falcon 9 launches ranges between $15 million and $30 million per mission, giving SpaceX a significant cost advantage over expendable rockets.

"2025 and 2026 are likely to represent the peak of Falcon launch activity, with the company planning to progressively shift missions to Starship."

- Stephanie Bednarek, VP of Commercial Sales, SpaceX

Looking forward, Starship is positioned as a major growth driver. By early 2026, the program has completed 11 full-stack test flights, with Flight 12 scheduled for April 2026. The Starship V3 variant, tested in March 2026, aims to cut launch costs to under $100 per kilogram while delivering over 200 tons to orbit - the equivalent of about 10 Falcon 9 launches combined.

xAI Merger Impact on Financial Growth

In a major development, SpaceX completed an all-stock merger with xAI in early 2026, valuing the combined entity at around $1.25 trillion. This merger integrates AI capabilities with space infrastructure, positioning xAI as a key customer for SpaceX's orbital platforms. The goal? To develop space-based AI data centers that leverage Starlink’s satellite network for AI operations.

Although xAI is expected to contribute less than $1 billion in revenue through 2026, the merger has significantly boosted SpaceX's market valuation. The combined entity is targeting an IPO valuation between $1.5 trillion and $2 trillion, with plans to raise $50–$75 billion - potentially the largest capital raise in history, though investors must navigate liquidity constraints common in private markets.

"The launch business and the Starlink business are proven, here and now. xAI is about optionality."

- Daniel Hanson, Portfolio Manager, Neuberger's Quality Equity Fund

However, this integration comes with high costs. SpaceX burned through $8 billion in cash during 2025 to fund a $20 billion data center project, which could lead to zero or negative GAAP earnings in the short term. The success of this venture hinges on Starship V3’s ability to enable cost-efficient launches for orbital data centers. Additionally, the merger supports the development of "Starlink Mobile", a potential device optimized for running high-performance neural networks instead of traditional smartphone functions. This opens up new revenue opportunities that align with SpaceX's long-term ambitions.

IPO Valuation and Market Potential

SpaceX is gearing up for what could be the largest public offering in history. The company submitted a confidential draft registration statement to the SEC on April 1, 2026, aiming for a June 2026 IPO. With a targeted valuation between $1.75 trillion and $2 trillion, SpaceX plans to raise up to $75 billion - more than double Saudi Aramco's $29.4 billion IPO record from 2019.

Valuation Targets and Price-to-Sales Ratios

SpaceX's valuation metrics are ambitious. Based on a projected 2025 revenue of $16 billion, the company is pricing itself at an estimated 109x trailing revenue. Looking ahead to 2026, with anticipated revenue of $25 billion, the trailing multiple adjusts to about 70x.

"A $1.5 to 1.75 trillion valuation would effectively price SpaceX as if it were already a mature mega-cap tech platform, not a capital-intensive aerospace company still proving its long-term profitability."

- Due.com Investment Analysis

The valuation is built on three main pillars: Starlink's subscription business (valued at $1.1 trillion), dominance in reusable rocket launches (approximately $400 billion), and potential gains from orbital AI computing following the xAI merger (around $250 billion). Starlink, with EBITDA margins estimated between 54% and 63%, has been a major factor in driving investor excitement. SpaceX's overall EBITDA multiple is around 220x, based on $8 billion in 2025 EBITDA - far surpassing Nvidia's peak AI multiple of 70x. These numbers highlight the strong investor sentiment surrounding the IPO.

Investor Confidence and Market Outlook

The market's confidence in SpaceX continues to grow, reflected in recent private transactions. A December 2025 private tender offer valued shares at $421 each, putting the company’s pre-merger valuation at $800 billion. Following the February 2026 xAI acquisition, which valued xAI at $250 billion, the combined entity's valuation climbed even higher. Analysts now see SpaceX less as a traditional aerospace company and more as a "LEO monopolist" or a hybrid between a telecom and SaaS platform, a perspective that supports its tech-like valuation multiples.

This optimism is further fueled by SpaceX's operational achievements. In 2025, the company captured over 80% of global orbital mass and completed 166 Falcon 9 and Falcon Heavy launches. Starlink's subscriber base surged from 4.6 million in late 2024 to over 10 million by early 2026, while its Direct-to-Cell service reached 16 million users, with a goal of hitting 25 million by the end of 2026. This shift from one-time launch revenue to recurring subscription income has been a key factor in boosting investor confidence.

The IPO will feature a dual-class share structure, allowing Elon Musk to retain 79–80% of voting control despite a diluted economic stake. The underwriting will be led by a 21-bank syndicate, including Morgan Stanley, Goldman Sachs, JPMorgan, BofA, and Citi. SpaceX also plans to allocate 30% of IPO shares to retail investors - an unusually high percentage. If the IPO proceeds as planned, SpaceX could join the Nasdaq-100 just 15 days after listing, thanks to updated 2026 index rules, potentially driving significant demand from passive funds.

For those looking to explore pre-IPO opportunities, the SpaceX Stock Investment Guide offers insights into private market investing, valuation trends, and strategies for accessing SpaceX shares before the IPO.

Financial Projections Beyond 2026

Revenue Scaling and Margin Growth

Looking beyond 2026, SpaceX has set its sights on extraordinary growth. The company plans to boost revenue from about $25 billion in 2026 to a staggering $150 billion by 2040, with EBITDA expected to climb to $95 billion. Achieving this scale will demand consistent execution across all its business segments.

At the heart of this growth is Starlink, the satellite internet service. By 2028, Starlink is projected to reach 50 million subscribers, potentially generating $40 billion annually. The upcoming Starlink V3 satellites, capable of 1 Tbps downlinks - a massive leap from the current 40 Gbps - will allow SpaceX to target high-revenue urban markets. While recent expansions into regions like India and Africa caused ARPU to drop by 50–70% compared to U.S. rates, the V3 rollout is expected to bring ARPU back up in developed markets by 2027–2028.

Another key driver is the commercialization of Starship. The Starship V3 orbital operations could tap into a $150 billion market, encompassing heavy-lift launches, in-orbit refueling, and point-to-point Earth transport. By reducing launch costs to $10–$100 per kilogram - a sharp contrast to Falcon 9's ~$2,700/kg - SpaceX could enable business models that were previously unfeasible. The company aims to scale to 100+ Starship flights annually by 2028.

Defense contracts through the Starshield program are also poised for growth, with annual revenue projected to rise from $5 billion to over $10 billion as space becomes a key focus for missile defense and intelligence.

While these projections outline a bold vision, they also highlight the challenges and risks tied to such ambitious goals.

Risks and Capital-Heavy Projects

Reaching these targets will require navigating significant financial and operational hurdles. In 2025, SpaceX's capital expenditures totaled $20.7 billion, surpassing its revenue of $18.5 billion. The development of Starship alone costs approximately $4 million per day, and building a fleet of 10,000 Starships is estimated at $350 billion.

"Taking SpaceX public now is a bet that he can marshal the resources now, during his lifetime, to make Mars City One a reality."

- Eric Berger, Author and Journalist

To justify the anticipated IPO valuation of $1.5 trillion to $1.75 trillion, SpaceX would need to achieve GAAP net earnings of around $80 billion by 2031 - a figure that surpasses the current earnings of many leading tech companies. Accounting expert Jack Ciesielski commented:

"Whether SpaceX can get there is really a moonshot. It's anybody's guess how big the space industry will become in the future."

The merger with xAI adds another layer of complexity. In 2025, xAI reportedly incurred $8 billion in losses, which could weigh on SpaceX's consolidated earnings in the near term. Furthermore, the $19.6 billion purchase of EchoStar spectrum, along with major investments in "Moonbase Alpha" and Mars colonization, represents massive financial commitments with uncertain timelines for returns.

Operational challenges also loom large. In 2025, Starship had a 40% recovery success rate (2 out of 5 missions), and delays in achieving "Version 3" orbital capabilities could disrupt NASA's Artemis lunar landing schedule and SpaceX's own plans for scaling. Regulatory hurdles, including FAA concerns about reentry debris and the impact of frequent launches on commercial aviation, add further complications.

The planned June 2026 IPO aims to raise $75 billion to support this capital-intensive roadmap. While Starlink's projected free cash flow of $5 billion to $8.1 billion in 2026 offers some financial buffer, the success of SpaceX's ambitious plans will depend on its ability to execute across multiple fronts, from Starship commercialization to Mars infrastructure and orbital AI computing. These challenges underline the delicate balance between visionary goals and disciplined pre-IPO execution.

Conclusion: What Investors Should Know

SpaceX's trajectory toward profitability in 2026 highlights a remarkable evolution - from a launch-focused operation to a high-margin space services powerhouse. The numbers tell the story: Starlink now accounts for about 70% of the company’s total revenue, with EBITDA margins soaring to 63%. These figures far outpace the typical 20% margins seen in traditional satellite operations, showcasing a fundamental shift in the company's business model.

In 2025, SpaceX achieved $8 billion in EBITDA on approximately $16 billion in revenue, reflecting a 53% margin and a significant move toward cash-flow positivity. This milestone sets the stage for 2026, with projected revenue between $27 billion and $30 billion and nearly $5 billion in free cash flow. By reaching cash-flow positivity, SpaceX reduces its reliance on external funding, allowing it to self-finance ambitious projects like Starship development and Mars infrastructure initiatives.

However, the road ahead isn’t without challenges. The company’s ambitious $1.75 trillion IPO valuation target hinges on flawless execution. With a 109× price-to-sales multiple, SpaceX must excel in expanding Starlink’s reach, unlocking Starship’s $150+ billion market potential, and successfully integrating the xAI merger. This valuation underscores not only the rapid pace of revenue growth but also the strategic reshaping of its core business operations.

Investors should also consider the company’s strengths: government contracts and a dominant market position provide stability, while Starlink’s subscription-based model ensures predictable cash flows. However, regulatory hurdles and the immense capital requirements of SpaceX’s bold projects remain notable risks.

For those exploring pre-IPO opportunities, understanding these trends is crucial. To dive deeper into SpaceX’s valuation and private market dynamics, visit SpaceX Stock Investment Guide for more insights. As 2026 approaches, SpaceX stands at a critical juncture, balancing its solid financial performance with the challenges of executing its most ambitious goals yet.

FAQs

How sustainable are SpaceX’s 60%+ Starlink margins as Starlink scales?

SpaceX’s Starlink is currently enjoying profit margins above 60%, thanks to efficient scaling, extensive vertical integration, and a steadily growing user base. However, maintaining these margins in the future could become more challenging. Increased competition and the need for higher capital expenditures are likely to put pressure on profitability as the business continues to grow and evolve.

What could derail the June 2026 SpaceX IPO valuation target?

The valuation target for SpaceX's anticipated IPO in June 2026 might face pressure if high valuation multiples don't align with the company's cash flow. This could happen if spending outpaces earnings or if Starship flights fail to meet expectations. Additional challenges include potential regulatory hurdles, political changes that could impact government contracts, and uncertainties surrounding key operations like Starlink and Starship. Together, these factors could cast doubt on SpaceX's ability to sustain profitability and achieve long-term growth.

How much does Starship success affect SpaceX’s long-term profitability?

SpaceX’s long-term profitability heavily depends on the success of its Starship program, but the outcome remains uncertain, given how early the program still is.

In 2025, SpaceX reported revenues between $15 billion and $16 billion, with the majority coming from Starlink. Starlink contributed $11.4 billion, boasting an impressive 63% EBITDA margin. While Starship holds enormous potential for the future, its current financial contribution is minimal. For now, SpaceX’s earnings rely heavily on Starlink and contracts with government agencies.

Comments ()