SpaceX Funding History: Founder Equity Impact

SpaceX raised billions across 30+ rounds while preserving founder control through dual-class shares, secondary sales, and strategic funding.

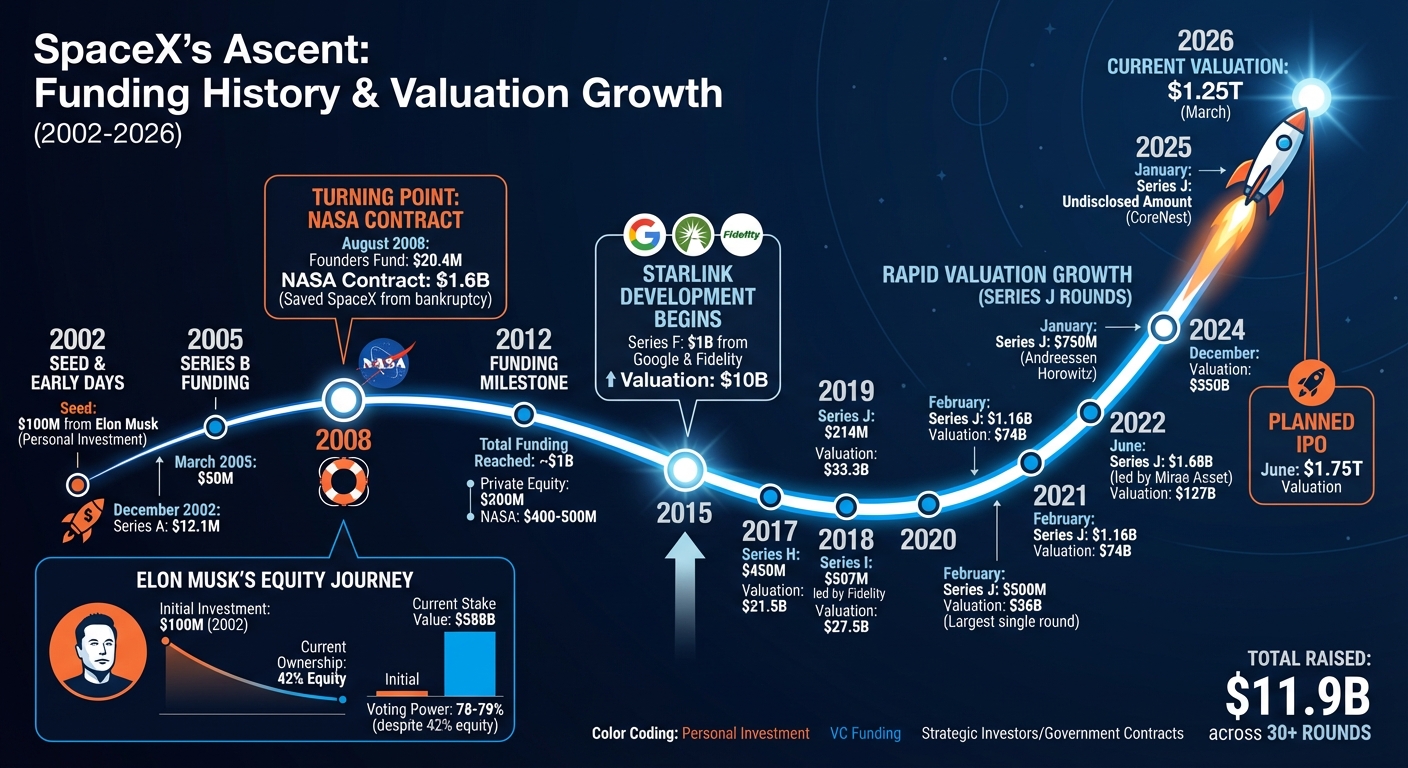

Elon Musk’s journey with SpaceX showcases how strategic funding and equity management can fuel massive growth while maintaining control. Musk initially invested $100 million of his own money in 2002, avoiding early reliance on venture capital. By March 2026, SpaceX had raised $11.9 billion across 30+ funding rounds, achieving a valuation of $1.25 trillion. Musk’s ownership, though diluted to 42%, is now worth $588 billion, thanks to the company’s exponential growth.

Key milestones include:

- 2008: NASA’s $1.6B contract saved SpaceX from bankruptcy.

- 2015: Google and Fidelity invested $1B, valuing SpaceX at $10B.

- 2020–2024: Series J rounds raised billions, growing valuation to $350B by 2024.

- 2026: SpaceX prepares for an IPO at a $1.75T valuation.

Musk retained control via dual-class shares, super-voting stock, and secondary sales. These strategies minimized dilution while ensuring his decision-making authority. The upcoming IPO will test whether public investors align with Musk’s governance approach, offering a rare chance to invest in SpaceX stock alongside institutional giants.

SpaceX Funding Timeline: From $100M Seed to $1.25T Valuation (2002-2026)

SpaceX's Funding History: Major Milestones

Early Funding Rounds (2002–2015)

SpaceX kicked off its journey with a hefty $100 million seed investment from Elon Musk. This funding was used to develop the company's first three rocket engines - Merlin, Kestrel, and Draco - as well as the Falcon 1 vehicle. The first official Series A round followed in December 2002, raising $12.1 million, with a $50 million Series B round coming in March 2005.

By May 2012, SpaceX had secured around $1 billion in total funding. Interestingly, only about $200 million of this came from private equity. The bulk of the funds - between $400–$500 million - came from NASA through progress payments on launch and development contracts. Founders Fund also played a key role, contributing $20.4 million in August 2008.

A major breakthrough occurred in January 2015 when Google and Fidelity Investments co-led a $1 billion Series F round. This round valued SpaceX at $10 billion and gave the investors an 8.333% stake. The funding supported the early development of the Starlink satellite constellation and bolstered SpaceX's ambitious goals. This early financial support laid the groundwork for future funding rounds that would significantly increase SpaceX's valuation and attract a broader pool of investors, many of whom must handle liquidity constraints inherent in private equity.

Major Funding Rounds and Valuation Growth (2017–2025)

After establishing a solid financial base, SpaceX entered a period of aggressive funding from 2017 to 2025. This phase saw the company achieve remarkable valuation growth, driven by advancements in reusable rocket technology and the expansion of the Starlink network. Each milestone not only brought in more capital but also reshaped the equity structure for its founders. For those looking to join these institutional rounds, there are several ways to invest in SpaceX before its IPO.

In July 2017, SpaceX raised $450 million in a Series H round, which valued the company at $21.5 billion. This was followed by a $507 million Series I round in April 2018, led by Fidelity, which pushed the valuation to $27.5 billion.

The pace quickened between 2020 and 2023, with multiple Series J tranches fueling the company's growth. The largest single round came in August 2020, raising $1.9 billion with participation from Legendary Ventures. In February 2021, SpaceX secured $1.16 billion from investors like Sequoia Capital, Valor, Coatue, and Fidelity, bringing its valuation to $74 billion. By June 2022, a $1.68 billion round led by Mirae Asset nearly doubled the valuation to $127 billion. Andreessen Horowitz (a16z) then stepped in with a $750 million investment in January 2023 to support the expansion of Starlink and launch operations. By December 2024, SpaceX's valuation had climbed to an estimated $350 billion.

| Date | Amount | Round | Post-Money Valuation | Key Investors |

|---|---|---|---|---|

| Jan 20, 2015 | $1B | Series F | $10B | Google, Fidelity Investments |

| Jul 26, 2017 | $450M | Series H | $21.5B | - |

| Apr 5, 2018 | $507M | Series I | $27.5B | Fidelity Investments |

| Jun 24, 2019 | $214M | Series J | $33.3B | Ontario Teachers' Pension Plan |

| Feb 28, 2020 | $500M | Series J | $36B | - |

| Aug 4, 2020 | $1.9B | Series J | - | Legendary Ventures |

| Feb 16, 2021 | $1.16B | Series J | $74B | Sequoia Capital, Valor, Coatue, Fidelity |

| Jun 13, 2022 | $1.68B | Series J | $127B | Mirae Asset, Space.VC, Kinetic |

| Jan 2, 2023 | $750M | Series J | - | Andreessen Horowitz (a16z) |

| Jan 21, 2025 | Undisclosed | Series J | - | CoreNest |

Founder Equity Dilution: Methods and Analysis

How to Calculate Founder Equity Dilution

Equity dilution happens when a company issues new shares, increasing the total share count and reducing the percentage ownership of existing shares. Here's the key formula to understand it:

New Ownership % = (Founder Shares / Total Shares After New Issuance) × 100.

While a founder's ownership percentage may drop, it doesn’t necessarily mean their stake loses value - especially if the company’s valuation grows significantly.

Dilution isn’t just tied to fundraising rounds. For example:

- Employee Stock Option Pools (ESOPs): Typically require setting aside 10–20% of the pre-money valuation.

- Convertible Instruments: SAFEs and convertible notes create new shares upon conversion, further diluting ownership.

Post-money SAFEs can lead to higher dilution compared to pre-money SAFEs. Why? Post-money SAFEs lock in an investor's ownership percentage, regardless of future share issuances.

"Early money is the most expensive you'll ever accept because your company has minimal value. That means each invested dollar purchases a larger stake." – EquityList

Ownership dilution is particularly steep in the early stages. Between pre-seed and Series A, founders often lose 40–60% of their initial ownership. Data from Carta in 2025 shows median founder ownership drops to 36.1% after Series A and 23% after Series B. Median dilution per round typically looks like this:

- Seed: About 19.5%

- Series A: 18%

- Series B: 14%

- Series C: 10%

By the time a company goes public, the median founder-CEO owns roughly 8–10%.

These calculations are crucial for understanding how funding rounds have reshaped founder control in companies like SpaceX, or how to buy SpaceX stock as an outside investor. Let’s break down how specific rounds impacted SpaceX’s founder equity.

Major Dilution Events

SpaceX’s history offers a clear example of how major funding rounds can reshape founder equity. One key moment was the January 2015 Series F round, when Google and Fidelity Investments invested $1 billion at a $10 billion valuation. This funding, which supported early Starlink development, significantly diluted founder stakes. It also marked a shift in SpaceX’s focus - from launch services to satellite communications.

Another pivotal event was the August 2020 Series J round, where SpaceX raised $1.9 billion from Legendary Ventures and others. For those looking to participate in such rounds, meeting pre-IPO investment minimums is a standard requirement. This was one of the largest single capital injections in the company’s history. Each billion-dollar round required issuing more shares, further diluting Elon Musk’s ownership. However, as SpaceX’s valuation soared - from $74 billion in February 2021 to $127 billion by June 2022, and an estimated $350 billion by December 2024 - Musk’s stake grew in absolute value despite the percentage reduction.

These funding rounds highlight how Musk retained control of SpaceX, even as his ownership percentage was reduced. It’s a balancing act between dilution and valuation growth, and SpaceX’s trajectory offers a fascinating case study.

SpaceX IPO Lures Investors Into Murky Private Deals

How Elon Musk Maintained Control Despite Dilution

Elon Musk has maintained tight control over SpaceX through a clever use of a dual-class share structure, which separates ownership from voting power. As of early 2025, Musk owns about 42% of SpaceX's equity but controls an impressive 78% to 79% of the voting power. This is possible because Musk holds super-voting shares, which grant significantly more votes per share compared to the Class A shares owned by other investors. This setup not only secures his authority but also enables other strategies to reinforce his control.

Looking ahead to SpaceX's anticipated IPO in 2026, the company is considering a structure where super-voting shares might carry 10 to 20 votes each, compared to just one vote for regular shares. This approach resembles the share structures used by Meta Platforms and Alphabet Inc.

"That's not so much that I could control the company, even if I go bonkers." - Elon Musk, Founder and CEO, SpaceX

Musk's influence is further bolstered by SpaceX's board, which includes key executives and investor representatives who align with his interests. To minimize dilution during funding rounds, SpaceX issues non-voting stock to new investors.

Beyond the share structure, Musk also relies on specific funding strategies to protect his control over the company.

Down Rounds and Their Effect on Founder Control

SpaceX has successfully avoided down rounds - funding rounds at lower valuations than previous ones - which often activate anti-dilution provisions. These provisions typically issue additional shares to early investors, which could dilute a founder's control. By sidestepping such rounds, SpaceX has shielded Musk from the challenges many founders face when companies falter.

Secondary Sales and Control Preservation

Musk's control isn't just about share structuring; strategic secondary sales also play a significant role. Since January 2023, SpaceX has shifted its focus away from primary capital raises, which issue new shares and dilute existing ownership, toward organized secondary sales. These tender offers allow employees and early investors to sell their shares without adding new equity, thereby preserving Musk's dominance. For example, SpaceX conducted major tender offers at $185 per share in December 2024, $212 per share in July 2025, and $421 per share in December 2025.

To further ensure control, SpaceX enforces its right of first refusal on secondary market platforms like Forge Global and Hiive, blocking unauthorized sales. In December 2024, SpaceX even executed a $500 million share buyback during a $1.25 billion tender offer, reducing the number of shares held by outside parties and further consolidating control.

Another strategic move was SpaceX's acquisition of xAI in February 2026. This all-stock merger preserved Musk's voting dominance by issuing Class A common stock to new shareholders, rather than super-voting shares, ensuring his 79% voting power remained untouched.

Conclusion: SpaceX's IPO Path and Founder Equity

SpaceX's funding journey tells a story of careful planning and strategic moves. Starting with a $12.1M Series A in 2002, the company has grown to an astounding $1.25T valuation by February 2026. This growth highlights how strategic funding decisions have allowed SpaceX to thrive while preserving founder control. Over the course of more than 30 funding rounds, Elon Musk has managed to retain approximately 42% equity through the use of a dual-class share structure.

By leveraging strategic secondary sales, the company has provided liquidity without issuing new shares, ensuring Musk's control remains intact. This method has been crucial in maintaining centralized leadership as SpaceX moves closer to its public offering.

The planned IPO in June 2026, targeting a $1.75T valuation and up to $50B in new capital, will test whether public investors are aligned with Musk's governance approach. The company is expected to stick with its dual-class share structure, allowing Musk to maintain his decision-making authority even as public shareholders come on board. This strategy reflects SpaceX's ability to balance rapid growth with strong founder leadership.

"Valuation increments are driven by progress on Starlink, Starship and global direct‑to‑cell spectrum." - Elon Musk, Founder and CEO, SpaceX

Additionally, the all-stock merger with xAI in February 2026 has further aligned Musk’s broader technological ambitions while safeguarding his voting power. For those curious about SpaceX's private market dynamics before the IPO, resources like the SpaceX Stock Investment Guide provide valuable insights into valuation trends and private equity strategies in the space industry.

FAQs

How did Musk keep control with only 42% ownership?

Elon Musk managed to retain control of SpaceX even though he owns just 42% of the company. He achieved this by using a dual-class share structure, which gave him about 79% of the voting rights. This setup ensures that he has a strong say in the company's major decisions.

What’s the difference between primary rounds and tender offers?

Primary rounds and tender offers serve very different purposes in the financial world.

Primary rounds involve the issuance of new shares to bring in additional capital. While this approach can dilute the equity of existing shareholders, the funds raised are typically directed toward growth, development, or strategic projects that drive the company forward.

On the other hand, tender offers focus on buying back existing shares, either by the company itself or an external party. These offers often come with a premium price and are not about raising new capital. Instead, they aim to reduce the number of outstanding shares, consolidate ownership, or provide a way to return value directly to shareholders.

How could the 2026 IPO change SpaceX’s voting structure?

The 2026 IPO could give SpaceX the opportunity to adopt a dual-class share structure. This setup would allow Elon Musk to maintain substantial voting control, even if his ownership stake diminishes. Companies like Meta and Alphabet have used similar arrangements to ensure their founders retain influence over major decisions.

Comments ()